The Stablecoin Flippening Is Showing Up in the Data

Last week we wrote that MiCA had pushed USDT off every licensed venue in Europe and that the squeeze would show up somewhere. It just did — in Visa's on-chain data, and faster than we expected.

Visa's analytics dashboard (built with Allium, and filtered to strip out bot loops, exchange shuffling and other fake throughput) recorded an all-time-record $1.79 trillion in adjusted stablecoin transaction volume in June — up 63% in a single month and 125% year-over-year. The first half of 2026 totaled $8.82 trillion, more than all of 2024 combined. Stablecoins, in other words, are having their biggest year ever.

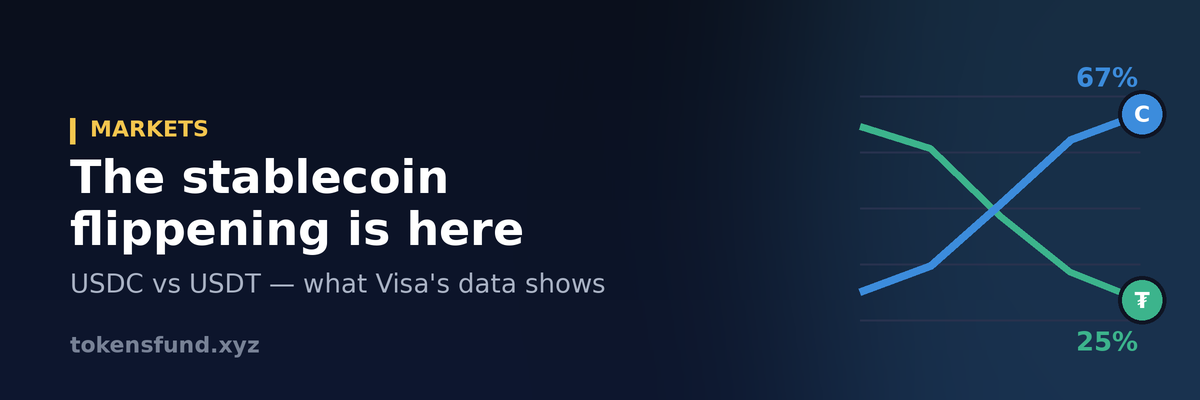

The headline inside the headline is who carried that volume. USDC moved roughly $1.21 trillion of June's total — about 67%. USDT moved around $573 billion. Across the half-year, USDC's share ran near 70% against roughly 25% for Tether — the widest gap ever recorded. Six years ago the same measurement showed the mirror image: in 2020, USDT handled nearly 90% of adjusted volume. The reversal is complete, and it's been consistent month after month, in every market regime.

Regulation drew the map

This didn't happen because traders woke up preferring Circle. It happened border by border. MiCA's reserve rules were terms Circle accepted and Tether refused — so when the July 1 deadline hit, USDC and EURC kept their EU listings while Coinbase, Kraken, Crypto.com and Binance's EU entity delisted or restricted USDT in the largest European delisting wave on record. In the US, the GENIUS Act's stablecoin licensing framework — final rules due this year — is one Circle is built to operate under and Tether, so far, is not.

Then the institutions followed the compliant rail. Standard Chartered now offers USDC minting and redemption through its banking infrastructure; BNY added USDC custody; Visa itself settles network obligations in USDC. When banks, payment networks and enterprise treasuries move money on-chain, they use the stablecoin their regulators recognize — by default, not preference. That's what June's volume is made of.

The honest caveats

Two things keep this from being a simple "USDT is dying" story — because it isn't.

- Volume is not market cap. USDT is still the giant: roughly $184 billion in circulation against USDC's ~$74 billion. The biggest stablecoin by supply and the biggest by real settlement volume are simply no longer the same coin.

- The market split into two markets. Look at transaction counts: USDT processed ~145 million transactions in June to USDC's ~57 million. USDT dominates high-frequency, small-value transfers — emerging markets, offshore dollar demand, people using it as money. USDC dominates large-value institutional settlement. They're increasingly not even competing for the same flows.

Worth one more line of skepticism: the dashboard is Visa's, and Visa has been a Circle partner since 2020. That said, USDC first passed USDT on this adjusted measure over a year ago and no major dataset has shown the opposite since — so the trend looks real even if you discount the referee.

What it means if you hold stablecoins

The practical read isn't "dump USDT" — it's that where you can use each coin is diverging, and your exits are worth planning around that:

- If you hold USDT in Europe, the licensed on/off-ramps have narrowed. Holding it remains lawful; converting it through a regulated venue is what got harder. Know your route out before you need it.

- If you're parking value long-term, understand you're now choosing between a bank-settled institutional rail (USDC) and an offshore liquidity rail (USDT) — different regulatory exposures, different failure modes. Neither is "safe"; they're differently exposed.

- Watch the next front: a 140-company consortium including Visa, Mastercard, Stripe and BlackRock just launched its own stablecoin (OUSD). The race USDT led for a decade is becoming a multi-front war, and flows will keep migrating with regulation.

Whichever way you rotate — USDT to USDC, stables into BTC or ETH, or back — you don't need a licensed venue or an account to do it. TokensFund swaps between them non-custodially: it compares THORChain, Chainflip, NEAR Intents, Changee and CCE.Cash and routes to the best rate, wallet to wallet, no KYC for standard swaps, flat 2% shown in the quote, automatic refund to your own address if a swap can't fill. The venue chokepoint is exactly the thing a wallet-to-wallet swap doesn't have.

A note on risk

Nothing here is financial advice. Stablecoins carry issuer, reserve and regulatory risk — including the ones with licenses — and the landscape is moving fast (GENIUS Act rules land this year; MiCA is already being reviewed). Figures above are from Visa's adjusted on-chain data as of July 7, 2026 and will move. You're responsible for using crypto lawfully where you live.

Rotate stables without a venue

Swap wallet-to-wallet →